hpo economic commentary, 4th quarter 2023

Have incoming orders already bottomed out?

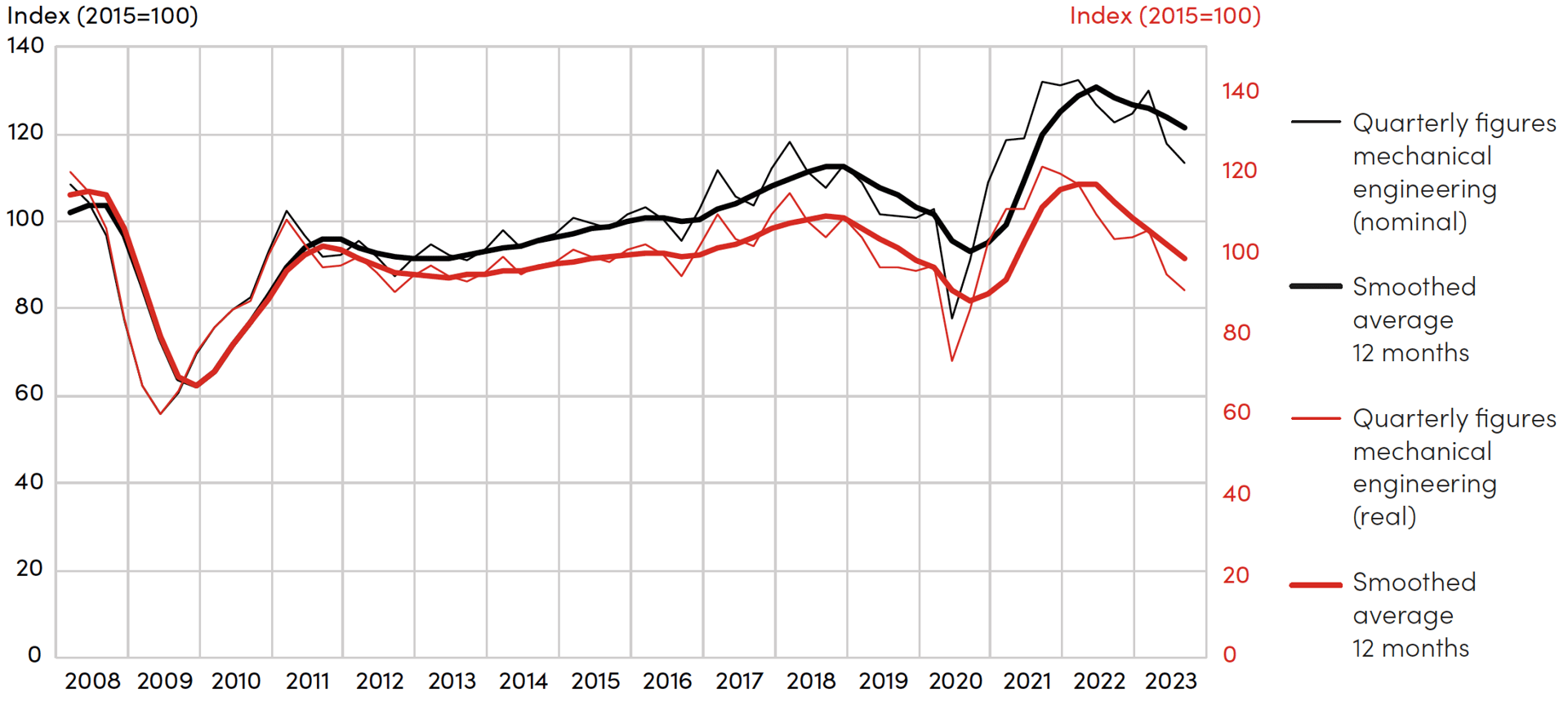

Incoming orders in the German mechanical engineering sector have been falling for six quarters, measured on an inflation-adjusted 12-month moving average.

Share article

Incoming orders in the German mechanical engineering sector have been falling for six quarters, measured on an inflation-adjusted 12-month moving average. The quarterly figures already peaked in the third quarter of 2021, since then incoming orders have fallen by more than 25 % (nominal: -14 %) and the trough still does not appear to have been reached.

Fig. 1: New orders in mechanical engineering in Germany (real and nominal)

Source: Raw data by Destatis, illustration by hpo forecasting

Mechanical engineering companies in other important manufacturing countries are also reporting falling order intake figures. Since the last peak, the nominal order intake of manufacturers in Japan has fallen by 15 % (with significantly lower inflation than in Europe) and in the United States by 6 %.

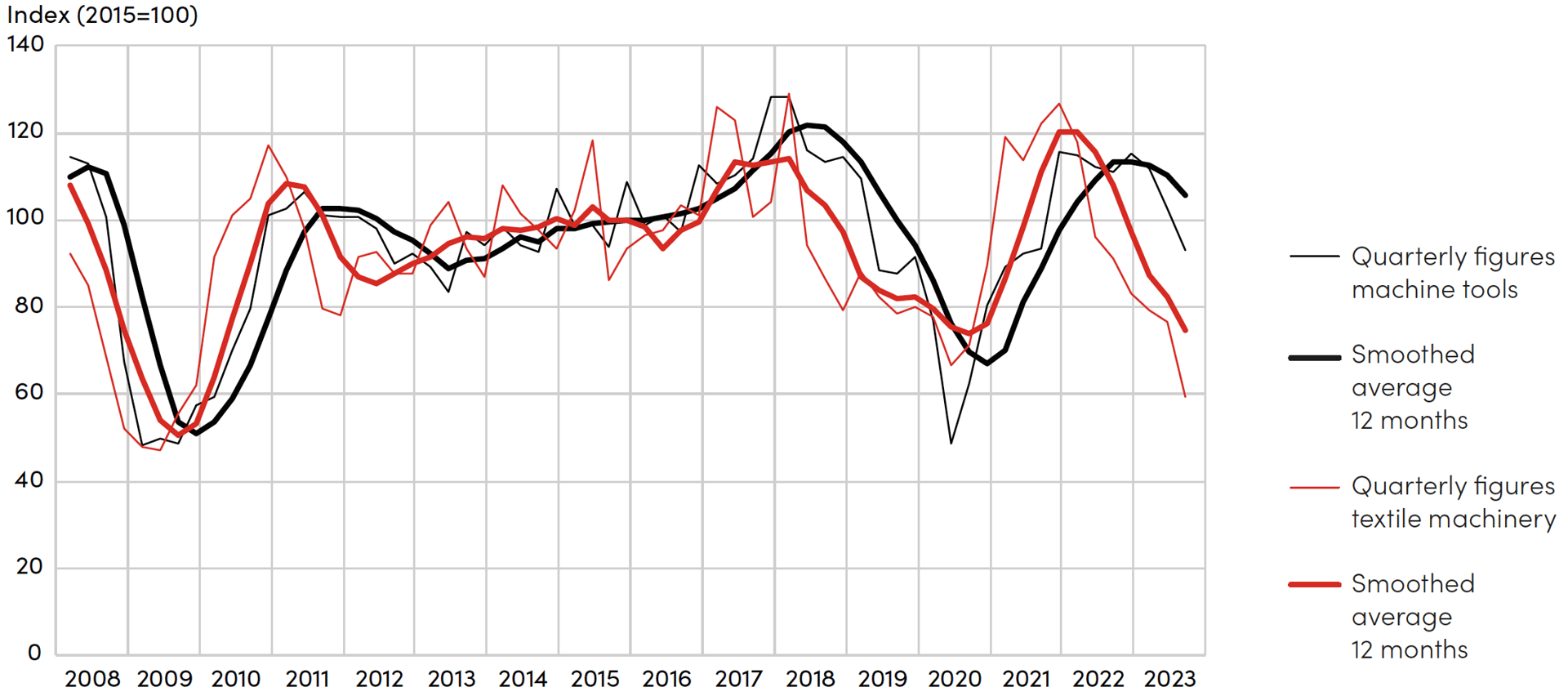

The correction is already enormous in some sectors. For German textile machinery manufacturers, a very early-cycle sector, Destatis figures show a decline in incoming orders of over 53 % since the peak in Q4 2021. In the first half of the year, it looked as if the bottom had been reached. However, the data for the third quarter dashed these hopes, as new orders fell by a further 22 % in nominal terms compared to the previous quarter to 59 index points. This is the lowest figure since the height of the financial crisis in 2009.

In numerous discussions held by hpo forecasting in September at EMO Hannover, the leading trade fair for production technology, many decision-makers from the machine tool industry were still confident. Strong demand was reported from the aircraft industry, medical technology and the defense industry in particular. However, the latest order intake figures from statistics offices and associations now show that the late-cycle machine tool industry is also being increasingly affected by the downward trend: According to Destatis, nominal order intake in Germany fell by 9.4 % (-10 % in real terms) in the third quarter compared to the previous quarter. This is the sharpest quarterly decline since the peak of the pandemic in the second quarter of 2020.

Fig. 2: Incoming orders for textile machinery and machine tools in Germany (nominal)

Source: Raw data by Destatis, illustration by hpo forecasting

“Automotive is dead,” said a CEO of a major machine tool manufacturer in an interview with hpo at EMO. It should be added that this applies above all to the combustion engine in cars. This is also illustrated by the weak business performance of the German automotive supply industry. Continental recently announced job cuts of around 5,000 employees in the Automotive division (this corresponds to around 5 % of the workforce).

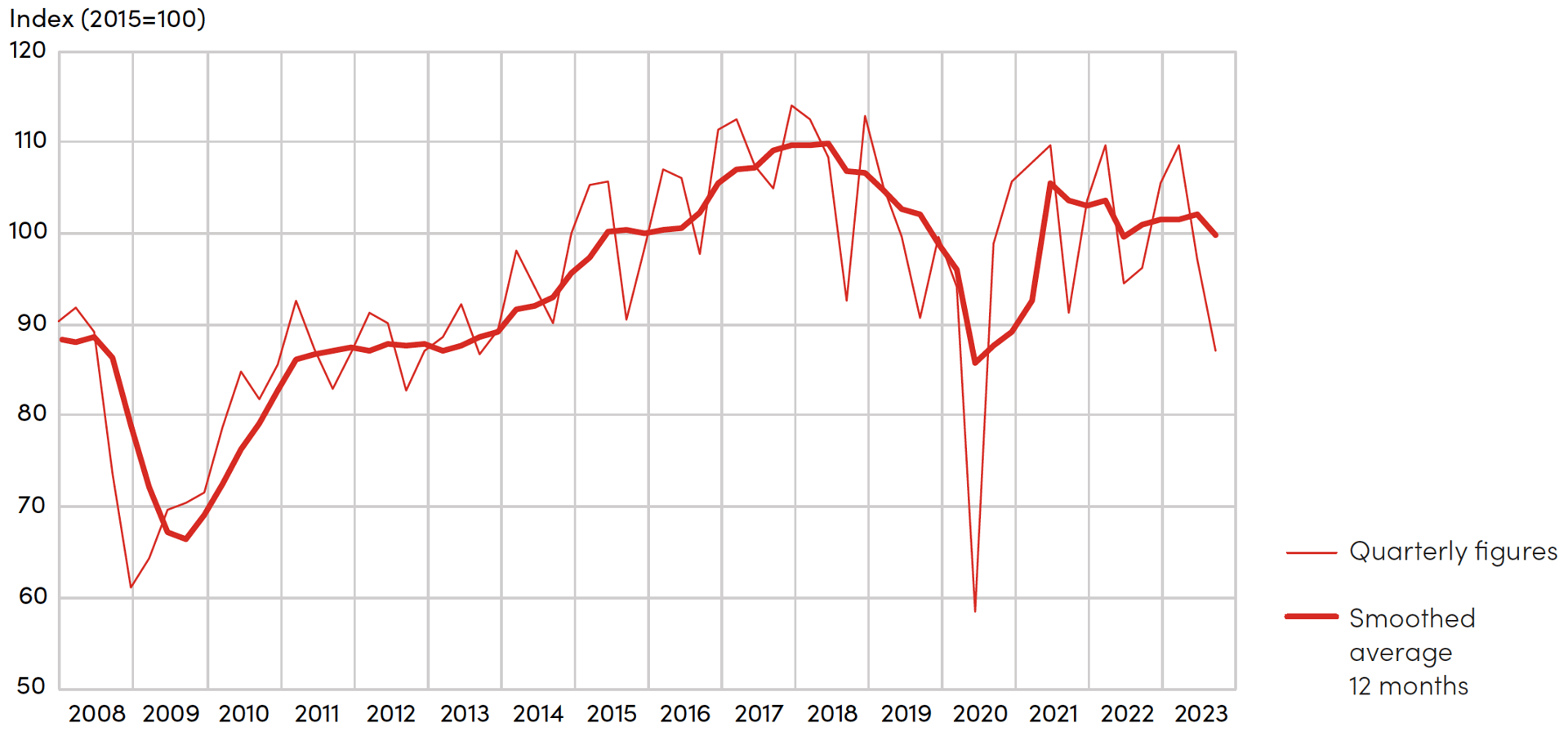

A look at the Destatis data confirms the picture: In the second and third quarters of 2023, incoming orders for manufacturers of motor vehicles and motor vehicle engines in Germany fell by more than 10 % in nominal terms compared to the previous quarter, partly due to seasonal factors. At 87 index points, incoming orders now reached their lowest level in nominal terms since the third quarter of 2012, with the exception of the second quarter of 2020, when many factories in Germany came to a standstill due to the pandemic.

Fig. 3: Incoming orders for manufacturers of motor vehicles and motor vehicle engines in Germany (nominal)

Source: Raw data by Destatis, illustration by hpo forecasting

While German car production is stuttering, Jörg Wuttke, the former and long-standing head of the European Chamber of Commerce in China, expects a “car tsunami” from China in an interview with The Market/NZZ.

China has built up enormous production capacities for electric vehicles in recent years, but the previously very steep growth curve in demand is now rapidly flattening. According to the China Association of Automobile Manufacturers (CAAM), the growth in battery electric vehicles sold in 2022 was still 85 % and fell to 27 % in the first eight months of 2023. Chinese car manufacturers are now pushing vehemently towards the European continent, as the American market is effectively closed to Chinese manufacturers due to protectionist measures. According to Wuttke, China has a car production capacity of 50 million cars per year, with domestic demand only absorbing around 23 million. Over the next few years, China intends to commission 120 new car carriers, each of which will be able to transport between 4,500 and 8,000 cars. This will result in a fierce predatory competition. However, the EU could follow the American example and also erect trade barriers. The Commission has already launched an investigation into whether China is subsidising its automotive industry using methods that violate World Trade Organisation rules.

The mood remains pessimistic

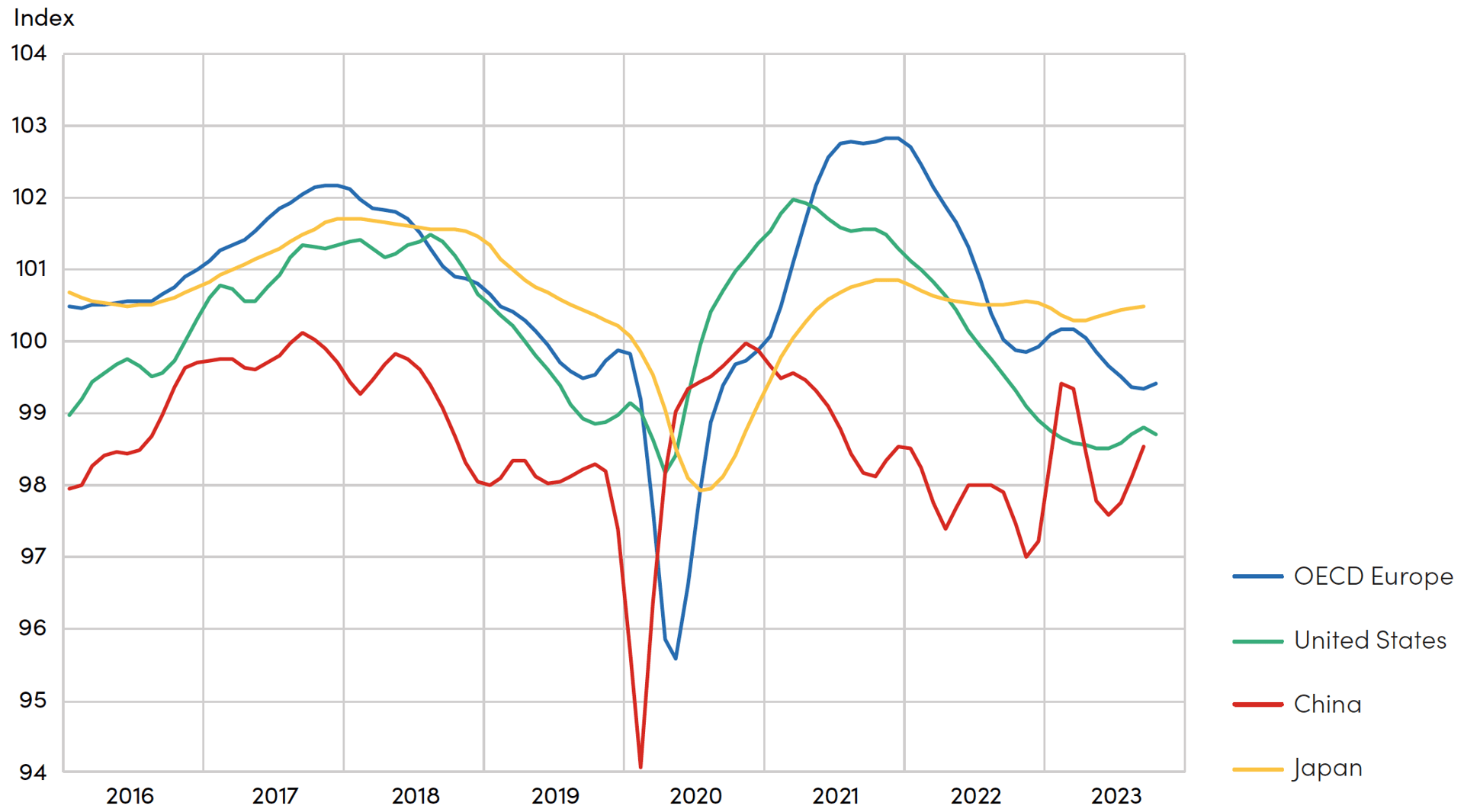

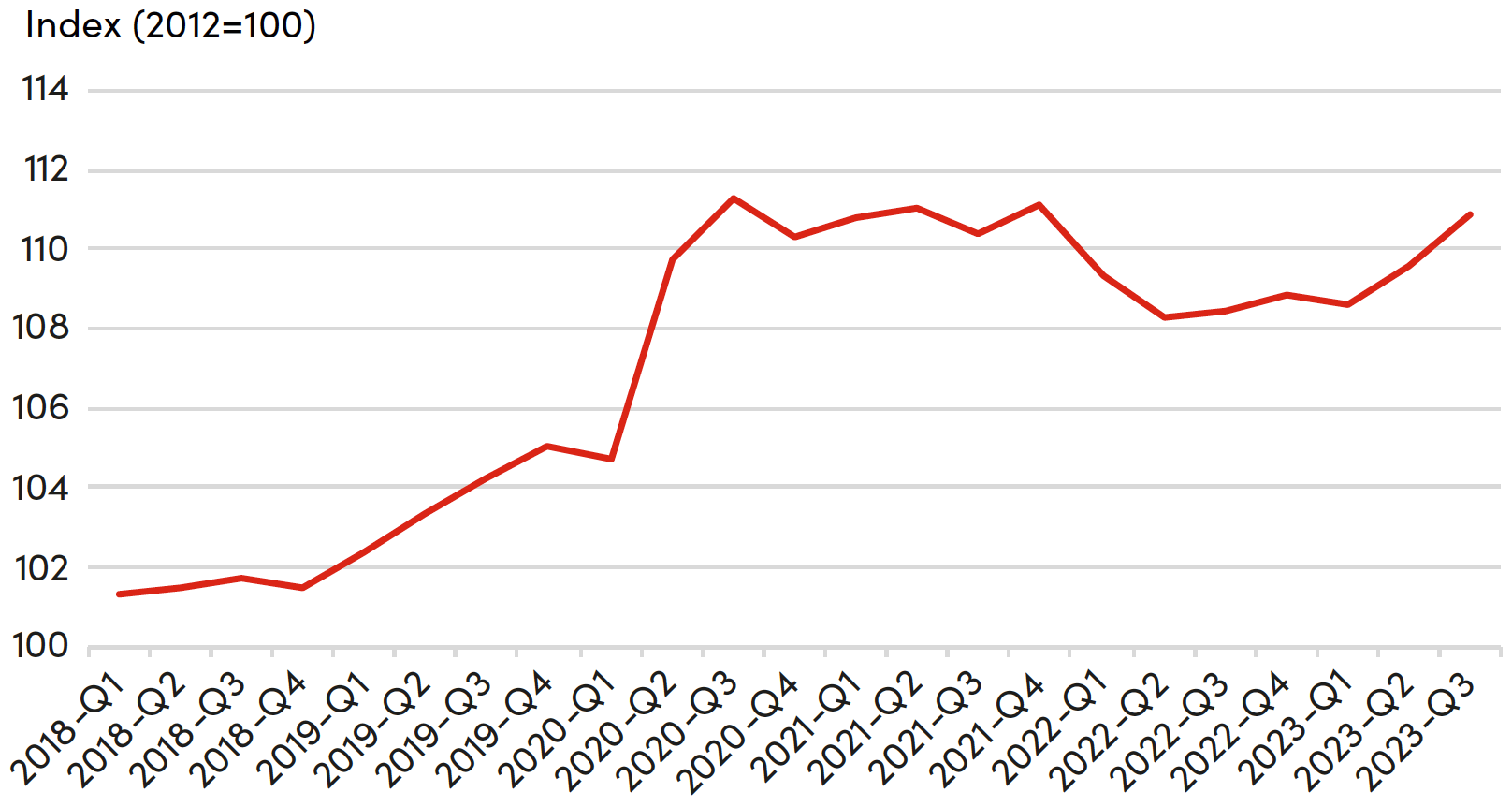

Due to the falling order figures, it is not surprising that the sentiment indicators also remain low in the contractionary range. The Business Confidence Index (BCI) published by the OECD confirms its quality as a leading indicator for the capital goods industry. The BCI remains clearly in contractionary territory in Europe, the United States and China (values below 100). The biggest change in recent months has been registered in China, where the mood has brightened somewhat. Industrial production in the Middle Kingdom has also been growing by around 4.5 % year-on-year for a few months now, with a slight upward trend.

Fig. 4: Business Confidence Index (BCI)

Source: Raw data by OECD, illustration by hpo forecasting

Consumer sentiment remains significantly more negative. In Europe and the United States, the value has fallen below 98 points again in recent months and is therefore lower than at the height of the pandemic. In China, the corresponding figure is a pessimistic 93 points. China has a real confidence problem, even at home.

The United States continue to surprise positively

American consumers are not letting the poor mood spoil their shopping fun, and this did not change in the third quarter: Retail sales rose by around 3.1 % year-on-year in nominal terms compared to the same quarter last year, starting from a still high level. The business magazine The Economist points out that, according to the latest statistics, American consumers are still sitting on surplus savings amounting to one trillion US dollars. They can therefore still afford a very low savings rate of 3.4 %. However, the level of consumer credit is also rising unabated to new highs almost every week. In the meantime, the credit default rate is also rising very rapidly, but fortunately still from a historically low level.

The US economy grew strongly in the third quarter (4.9 % annualised) and at the same time the unemployment rate rose from 3.5 % in July to 3.9 % in October. How does this fit together? The obvious conclusion is that labour productivity has risen. This has stagnated over the past three years and even declined at times. However, labour productivity in the United States has been rising significantly for around two quarters, most recently by 4.7 % quarter-on-quarter. This is the highest growth rate since 2020. Observers still disagree on the causes of this sudden productivity growth. One common theory is the productivity-boosting effect of the widespread use of artificial intelligence and large language models such as Chat GPT in everyday working life. If Americans manage to keep productivity growth high, this would also support economic growth in the coming year.

Fig. 5: Labour productivity in the non-agricultural private sector in the United States

Source: Raw data by Federal Reserve St. Louis, illustration by hpo forecasting

Nevertheless, the sources of danger for the US economy remain acute: the cost of strong growth is still being borne by very high government deficits. The Economist has calculated that in the 12 months to September, a government deficit amounting to 7.5 % of gross domestic product (GDP) was accumulated. With every loan that the US Treasury has to renew, interest costs rise sharply and put further pressure on government finances.

hpo forecasting maintains its assessment that GDP in the United States will fall significantly again in the coming quarters, as the higher key interest rates will gradually have a dampening effect on the real economy. Large companies, which often concluded long-term loan agreements during the low-interest phase, are less affected for the time being. Smaller companies very often only have short loan terms, as Marc Dittli from The Market/NZZ explains. These companies are feeling the effects of the restrictive financing conditions earlier than large corporations.

The financial markets are now assuming that interest rates have peaked in the current cycle. However, with core inflation remaining high at 4 % in October, it is still too early to hope for a reduction in key interest rates in the near

future. Financing conditions for companies and consumers will therefore remain challenging for the time being.

Direct investments in China collapse

At the beginning of November, the news made headlines that foreign direct investment in China was negative for the first time since data recording began in the 1990s: Foreign companies withdrew more capital from China than they invested for the first time in the third quarter of 2023. This suggests that foreign investment activity in China is very restrained. Many companies are waiting to see what direction the Chinese government takes. However, due to the high level of interest rates in the United States, a lot of capital is also being repatriated by foreign companies in order to invest it risk-free on the Western financial markets.

Large companies cannot afford to leave the second-largest economy; the market is too large, too dynamic and too important for that. According to numerous observers, many companies are pursuing the China for China strategy and are trying to establish alternative production sites in other countries. However, as China is also of central importance as a supplier for numerous industries, a genuine decoupling of China remains illusory for the foreseeable future.

China’s GDP grew by 4.9 % year-on-year in the third quarter. This should enable the targeted growth of 5 % to be achieved this year. However, maintaining the same level of growth in the coming year will be significantly more challenging, as the basis for comparison with the previous year and the widespread coronavirus lockdowns at the time was low in 2023. This favourable base effect will no longer apply next year. If the economies in Europe and the United States continue to cool down, this will also put the brakes on China’s important exports.

On a positive note, there are signs that the Chinese government is once again pursuing a more business-friendly policy. These include a 17-point plan to promote private investment and steps towards a slight easing of relations with important trading partners such as Australia, Japan and the United States. On the other hand, most observers agree that the measures introduced so far to stabilise the economy will not be nearly enough to overcome the current weak growth. The confidence of consumers and companies is still severely damaged and it will take time to regain this confidence. However, this is the prerequisite for China to boost domestic consumption. The savings rate of Chinese consumers is traditionally very high, so there is potential to significantly increase consumption. For this to happen, however, the very rudimentary social security network would have to be greatly expanded, among other things. There is currently no evidence of such a development. In addition, the main problem facing the Chinese economy remains the acute real estate crisis, with 80 to 90 million vacant apartments and a massive slowdown in construction activity. Around 65 % of Chinese private assets are tied up in real estate. If property prices fall, this has a correspondingly strong impact on the purchasing power of private households. An end to this crisis is not yet in sight.

If we consolidate the global economic development of recent months and the longer-term trends, the hpo forecasting team maintains its assessment that further setbacks in incoming orders in the capital goods industry are very likely. Apart from a few exceptions, there are still no signs of a trend reversal in the real economy.